Table of Contents

")

Nature

Cryptocurrency is an intriguing and unique asset class. As a contrarian investor I aim to buy when others are “non-believers” such as in 2016, before the bull market of 2017. In addition, I sell when everyone is buying. For example, in my private investing group, I told everyone I was selling my Bitcoin in February 2021. Although, I didn’t time the top and could have held on for ~30% more gains, I also missed the 66% plummet from all-time highs from November 2021. However, now the technical charts say Bitcoin has bottomed (for now) and the asset has even had its best month since 2021, with the price up ~20% over July.

Marathon Digital (NASDAQ:MARA) is a leading Bitcoin Mining company which acts as a leveraged way to play Bitcoin. As I mentioned previously, the price of Bitcoin popped by 20% in July (Blue line), however, Marathon Digital (orange line) is up a blistering 134% over that same period.

Marathon Digital (Orange) Vs Bitcoin (Blue) (created by author TradingView)

The technicals show bullish momentum signs for Crypto and thus I think it’s worth diving into Marathon Digital Holdings. A company which has bold management and big plans for future growth. Let’s dive into the Business Model, Growth Plans and my price targets for the juicy details.

Business Model

Marathon Digital aims to build one of the largest Bitcoin mining operations in North America. Its mining operations are based in Texas (hosted by Compute North), Montana (hosted by Beowulf) and South Dakota/Nebraska (hosted by Compute North).

Bitcoin Mining Operations (Investor Presentation)

In Texas, the company is building out and expected to deploy over 100,000 S19 Miners. An S19 is a purpose build mining computer (manufactured by Bitmain). In the Texas facility, the S19s can mine Bitcoin at a rapid 10 EH/s (10 Exahashes per second), where one exahash equals one quintillion hashes. For the uninitiated the “Hash Rate” is basically the speed of mining computed in “Hashes Per Second”. This is how fast the mining computer can solve the encrypted puzzle for that block.

To add some realism to this whole setup I have included a picture of one of the machines, so you can visualise what the setup would be like. Imagine 100,000 of these machines strapped together in a big warehouse.

Antminer S19 (Bitmain)

Green Mining is a Competitive Advantage

A key element of the company’s strategy is its focus on Bitcoin Mining powered by Renewable Energy sources. For example, its largest facility in Texas has 100% carbon neutral mining operations. This is predominately powered by wind and solar farms across the US. They also plan to transition out of its Hardin facility in the third quarter of 2022, to an area of more sustainable power. Powering mining operations from renewable energy sources is a big deal, given global Bitcoin Mining consumes more electricity than the country of Argentina! This equates to a 150 terawatt hours of electricity per year.

Given the international battle against climate change and the number of ESG (Environment, Social, Governance) funds, Bitcoin mining has to become sustainable. For example, Shark Tank Investor Kevin O Leary reported in 2021 he won’t buy “Bloodcoin” referring to Bitcoin mined from non-renewable energy sources, in a direct quote he stated;

“We have compliance on large institutions, we have covenants on how assets are made, whether carbon is burned, whether there are human rights involved, whether it’s made in China.” – Kevin O Leary

This leads to a powerful conclusion that all Bitcoin is not equal. Bitcoin mined from sustainable sources could potentially be worth more than Bitcoin mined from other less “Green” or unverifiable sources. Bitcoin ETF’s, institutional investors and even companies which may want to own Bitcoin on their balance sheet will thus likely be inclined to buy “clean coins”. As Marathon Digital has verified Carbon neutral US locations, this could give them a competitive advantage.

Lowering Mining Costs

Part of management’s strategy is to “de-risk” the business by becoming more resilient to the potential declines in the price of Bitcoin. Management plans to do this by leveraging its scale to negotiate favorable contract terms and being agile as Bitcoin rises and falls. Another method they can “de risk” operations and improve their margins is by cooling down its machines in an efficient manner. As all that computing power generates vast amounts of heat and thus cooling is a key electricity consumer.

Immersion cooling its miners via a dielectric liquid is something management has spoken of in the past. The company forecasts this could result in greater efficiency and the ability to overclock (run GPU faster than standard speed) by up to 40%. However, it should be noted that to set up such an immersion cooling system is expensive and the proof it will work is not defined.

Growth Strategy

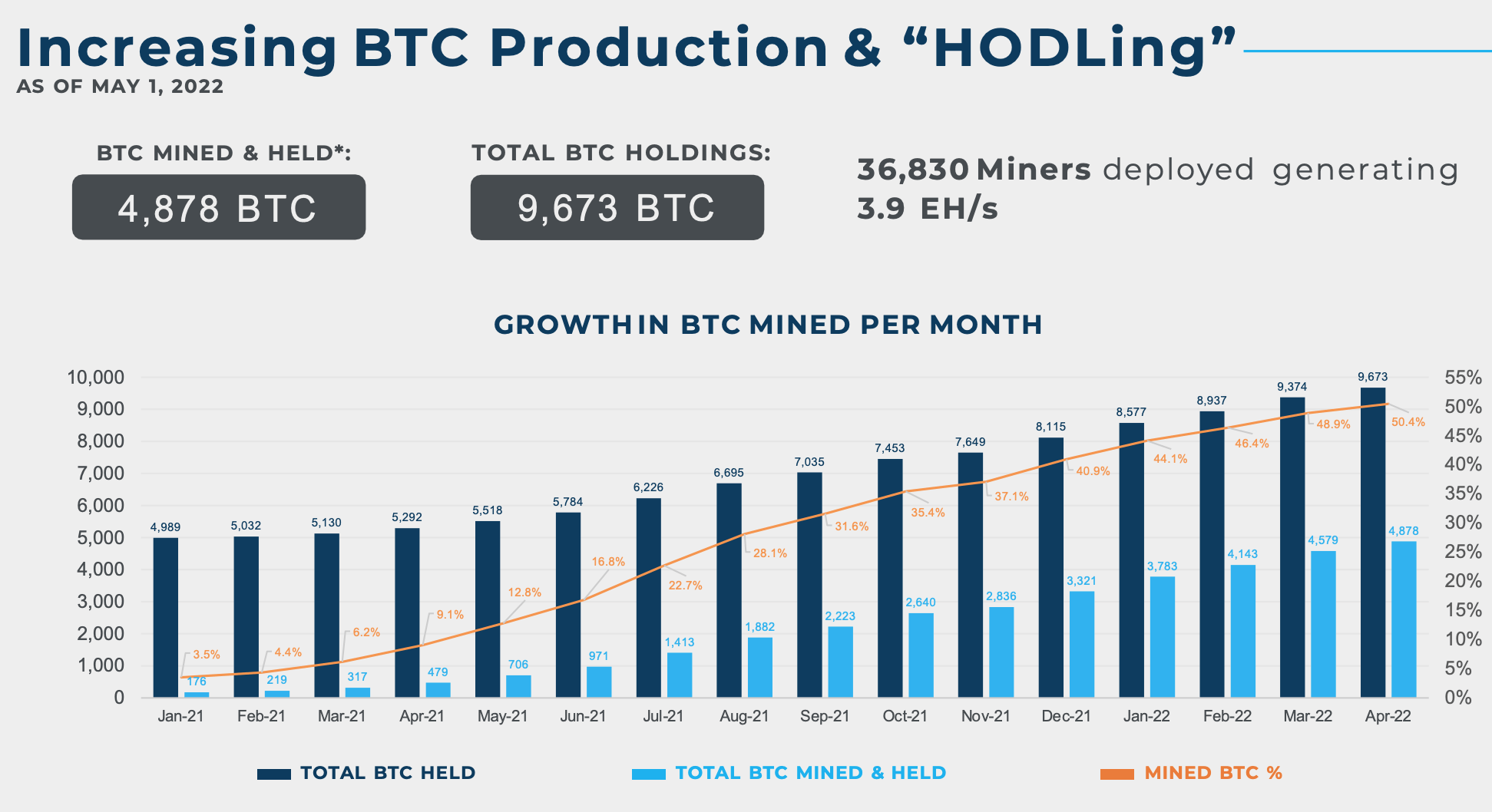

Marathon Digital’s growth strategy involves improving Bitcoin production by increasing the hash rate (speed of mining). As you can see from chart below the company has increased its Bitcoin production over time and are holding the asset given the volatility. It was interesting to see the company has a sense of humor as they referred to the “HODLing” of Bitcoin, perhaps appealing to their retail investor base.

MARA Bitcoin Mining (Investor Presentation)

As of the first quarter of 2022, MARA produced 1259 Bitcoin which was an increase over 1,098 BTC in the prior quarter and was higher than other Bitcoin mining companies in the industry. At the time of writing the company has 36,830 miners deployed at a 3.9 EH/S speed. As mentioned prior, the Texas facility currently has up to 10 EH/S of mining speed and the company estimates it can grow its overall hash rate to 23 EH/S which is rapid.

Management also has bullish growth plans to scale its Bitcoin miners from ~37,000 machines to over 200,000 machines by the second quarter of 2023. These are bold plans but historically management has struggled to keep up with its own targets. The good news is they recently scored a win in late July 2022, as they secured capacity for approximately 200 megawatts from Applied Blockchain (NASDAQ:APLD).

Value of Bitcoin Holdings?

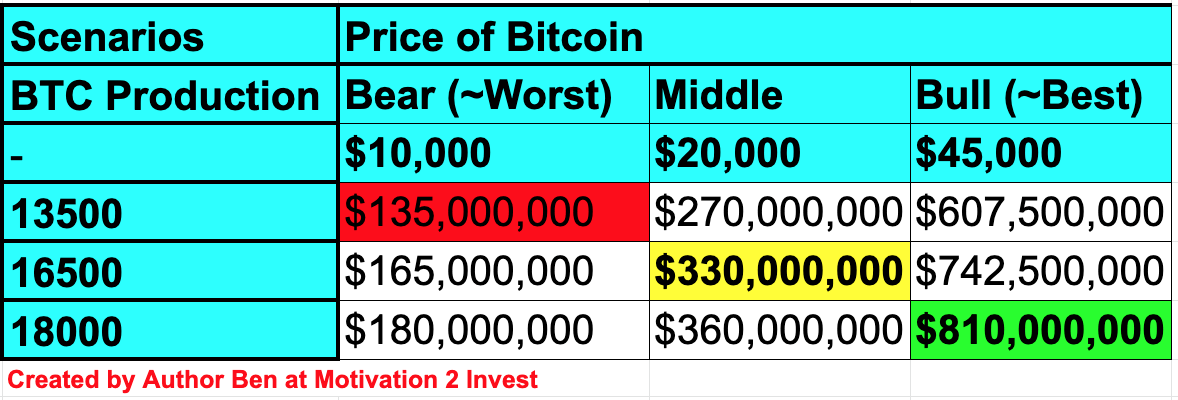

Knowing where the price of Bitcoin will be in the future is extremely difficult to forecast and knowing the true value of it, is pretty much impossible to calculate. However, we can look at a few scenarios of different Bitcoin prices and then estimate the value of Marathon’s holdings from this. On the table below you can see I have extrapolated out its total held Bitcoin of 9,673 Bitcoin as of Q122 with various growth rates and scenarios for Bitcoins price.

In the “Worst” case (Red), the company produces only slightly more Bitcoin than in Q122 and Bitcoin gets sliced in half to $10,000 (July 2020 price). Given the ecosystem which has built up around Bitcoin over the past couple of years and the number of companies who have added Bitcoin onto their Balance Sheet since then, I deem this scenario to be unlikely but not impossible. That would value the fund’s holdings at a mere $135 Million.

Given the “Best” case scenario Bitcoin skyrockets back to its April 2022 level of $45,000 and the company increases its production speed to result in 16500 Bitcoins held, valued at ~$810 million. Again, I don’t believe this case to be likely in the short term to give the “risk-off” appetite of investors but longer term it’s a possibility. Thus if we take the middle scenario of $20,000 for the price of Bitcoin, which is slightly less than the $23k BTC price at the time of writing and then production steadily increases speed, MARA would hold 16,500 Bitcoins valued at ~$330 million. At a market cap of $1.38 billion at the time of writing this would value it at four times its Bitcoin value.

Bitcoin Estimates MARA (created by author Ben at Motivation 2 Invest)

If I convert the prior calculation over to an approximate price target I get ~$8/share in the worst case, ~$13.50/share in the mid range and $27/share at the high end. Given, current price is ~$13/share I deem the stock to be a “HODL,” I mean “HOLD” at the time of writing.

Risks

Financial Perspective

Marathon Digital has bold plans, but remember this is based on future estimates. In the trailing 12 months the company produced just $193 million in revenue, with $13 million in gross profit and -$46 million in operating income. Given the company has a market capitalization of ~$1.38 billion, this is a Price to Sales of ~6.83 according to Seeking Alpha. This isn’t exactly cheap, but it is 83% cheaper than its 5-year mean price.

The company does have a strong cash position of $336 million in cash and short term investments. However, $729 million in long term debt is fairly high given the net income is negative.

Recession

Bitcoin in theory should be a hedge against Inflation, but so far that correlation has not played out. Historically Bitcoin and Bitcoin mining stocks have traded like risky growth stocks. The rising interest rate environment has caused a major devaluation in many growth stocks and thus retail investor appetite has been subdued. Block (SQ)(Square) saw its Bitcoin trading revenue in its cash app plummet in the last quarter.

When people are “feeling rich” they are happy to invest into speculative assets, but when people have their living costs such as Food and Energy squeezed by inflation, saving money becomes a priority.

Final Thoughts

Marathon Digital is an established player in the crypto mining industry. Its management is bold and forecast huge growth in the future. The success of this stock will be based upon two factors, the first is management’s ability to execute on its growth plans, the second is the price of Bitcoin. The multiple scenarios I laid out show the stock is trading at the middle case scenario for both Bitcoin price (after the recent rally) and production estimates. However, the financials are still based on future estimates and thus the stock is suited for a place in one’s speculative portfolio or as a trading asset, but after the recent rally it might be worth holding until the next earnings announcement for the second quarter of 2022.

More Stories

Top Cryptocurrencies for 2018: What Are the Best Bitcoin Alternatives?

Short History of Bitcoin

Bitcoin Mining & Security, Part 2